|

|

|

|

Original Article

The Influence of Social Factors and Subjective Norms on Investment Decision-Making: A Comparative Analysis of Gen Z and Millennials

|

Surbhi 1, Dr. A. K. Govilla

2 1 Research Scholar, Department

of Economics, Malwanchal University, Indore, India 2 Supervisor, Department of Economics,

Malwanchal University, Indore, India |

|

|

|

ABSTRACT |

||

|

Investment decision-making is increasingly influenced by social surroundings, especially in an environment shaped by digital media, peer interaction, family guidance, and widespread access to financial information. The present study examined the influence of social factors and subjective norms on investment decision-making among Gen Z and Millennial respondents. The study was based on primary data collected from 480 respondents and analyzed using SPSS and SmartPLS 4. The findings show that social factors significantly influence investment decision-making directly and also affect perceived behavioral control and subjective norms. Subjective norms also significantly influence investment decision-making in both generations. However, the multigroup analysis indicates that the path differences between Gen Z and Millennials are not statistically significant. The study concludes that social influence is an important determinant of investment behavior, but this influence operates in a broadly similar way across both generations. These findings support earlier literature highlighting the relevance of social influence, behavioral context, and normative pressure in financial decision-making Alshebami and Aldhyani (2022), Ikhsan and Wulandari (2024), Singh et al. (2025), Thanki et al. (2025). Keywords: Social Factors, Subjective Norms,

Investment Decision-Making, Gen Z, Millennials, Comparative Analysis,

Behavioral Finance |

||

INTRODUCTION

Investment

decision-making has become an increasingly important area of research because

financial participation is no longer shaped only by income, savings, and market

opportunity, but also by the broader social environment in which individuals

receive and interpret financial information. In the present era, people are

continuously exposed to investment-related messages through family discussions,

peer interaction, social media, online platforms, financial news, and expert

commentary. As a result, investment behaviour is increasingly influenced by

social surroundings, shared opinions, and perceived approval from others rather

than by purely individual reasoning. This changing context has made social

factors and subjective norms highly relevant constructs in explaining why and

how individuals make investment decisions Alshebami

and Aldhyani (2022), Tabassum et al. (2021),

Shahzad

et al. (2024). Social factors refer to the influence of

external environments such as family, peers, media, internet-based information,

and professional advice on financial thinking and action. These factors can

shape how individuals understand investment opportunities, assess risk, and

develop confidence in decision-making. In modern financial markets, especially

those supported by digital technology, people often rely on social sources to

validate information and reduce uncertainty before investing. Prior research

has shown that social influence is strongly associated with financial behaviour

and can meaningfully affect decision outcomes, especially when individuals are

still developing investment experience or depend on external guidance Alshebami

and Aldhyani (2022), Ammar et

al. (2025). This suggests that investment decisions

should be understood not only as rational economic choices but also as socially

embedded behaviours.

Alongside social

factors, subjective norms have also emerged as an important determinant of

financial and investment behaviour. Subjective norms refer to the perceived

approval, expectation, or pressure that individuals feel from important others

regarding whether they should perform a particular behaviour. In the investment

context, such norms may arise when family members, friends, colleagues, or

online communities encourage stock market participation, mutual fund

investment, or other financial activities. The literature rooted in the Theory

of Planned Behavior has consistently shown that subjective norms can influence

behavioral intention and decision-making, particularly in contexts where social

validation matters Ikhsan

and Wulandari (2024), Singh et

al. (2025), Thanki

et al. (2025). Similarly, Natalia

and Sihombing (2025) and Rahmayanti

et al. (2025) found that subjective norms contribute

meaningfully to investment intention, indicating that investment behaviour is

partly shaped by social approval and shared financial culture. The relevance of

these constructs becomes even stronger when examining Gen Z and Millennials,

two generations that are highly visible in today’s financial environment. Gen Z

has grown up in a deeply digital world where financial ideas, stock tips, and

investment trends circulate rapidly through social media, short-form content, and

peer networks. Millennials, while also digitally connected, often combine this

exposure with broader financial responsibilities, greater work experience, and

more practical engagement with long-term financial planning. Although both

generations are active participants in modern information ecosystems, the

strength and form of social influence may differ according to age, life stage,

financial maturity, and decision context Kurniadi

and Herdinata (2024), Shahzad

et al. (2024). Therefore, comparing Gen Z and Millennials

provides a useful basis for understanding whether social influence on

investment behaviour is generation-specific or broadly similar across cohorts.

A growing body of

research has examined investment behaviour using financial literacy, behavioral

finance, and planned behavior perspectives. Studies such as Arora

and Chakraborty (2023), Hussain

et al. (2022), and Suresh

(2024) have shown the importance of financial

literacy in shaping investment decisions, while other studies have emphasized

behavioral and attitudinal determinants such as risk tolerance, overconfidence,

and financial capability Adil et al. (2022), Ahmad

and Shah (2022), Song et al. (2023). However, several recent studies have also

stressed the importance of social and normative influences. Ikhsan

and Wulandari (2024), Singh et

al. (2025), and Thanki

et al. (2025) highlighted the relevance of subjective norms and planned behavior

variables in investment-related intention, while Ammar et

al. (2025) drew attention to the role of peer influence

in the financial decision process. These studies suggest that the social side

of investment behaviour deserves closer attention, especially in comparative

generational research. Despite this growing literature, there remains limited

empirical work that specifically examines the combined influence of social

factors and subjective norms on investment decision-making while directly

comparing Gen Z and Millennials in a single framework. Much of the existing

literature either focuses more heavily on financial literacy and personal

capability or examines social and normative variables in relation to intention

rather than actual decision-making. The present study addresses this gap by

focusing more directly on how social factors and subjective norms shape

investment decision-making and whether these effects differ significantly

across the two generations. This makes the study valuable both theoretically

and practically, as it adds to the behavioral finance literature while also

offering insights relevant for financial educators, policymakers, and digital

investment platforms.

The study is based

on the view that investment behaviour in the current era is shaped by an

interaction between social exposure and perceived social approval. Individuals

do not merely assess returns and risks in isolation; they also interpret what

others are saying, what others are doing, and whether investing appears

socially supported or expected within their environment. In this sense, social

factors may influence investment decisions directly, while subjective norms may

serve as a more specific social-psychological channel through which that

influence is expressed. By comparing these mechanisms across Gen Z and

Millennials, the study seeks to clarify whether the same social logic operates

similarly for both groups or whether generational differences meaningfully

alter the investment decision process.

Review of Literature

Social Factors and Investment Decision-Making

Social factors

refer to the external influences that shape an individual’s attitudes,

preferences, and actions in financial matters. These factors usually include

family opinion, peer influence, professional advice, media exposure,

internet-based information, and broader social interaction. In the context of

investment, social factors become important because investors often do not rely

only on personal judgment; they also consider what others are saying, doing,

and recommending before making financial decisions. Earlier studies have shown

that social influence plays an important role in financial behaviour and

investment-related action. Alshebami

and Aldhyani (2022) explained that social influence significantly affects financial

behaviour, especially among younger individuals, because financial actions are

often shaped by interaction with others and by the surrounding financial

environment. Ammar et

al. (2025) also highlighted that peer-related influence

contributes to investment decision processes and may shape how investors

interpret opportunities and financial choices. Tabassum

et al. (2021) found that behavioral and environmental factors, including

external influence, significantly affect investor decision-making behaviour.

These findings suggest that social surroundings can affect investment

decision-making by guiding attention, reinforcing ideas, and reducing

uncertainty. For Gen Z and Millennials, this influence is especially important

because both groups are highly connected to digital media, financial content,

and social communication networks.

H1: Social

factors have a significant positive effect on investment decision-making.

Social Factors and Subjective Norms

Subjective norms

refer to the perceived social pressure, approval, or expectation that

individuals feel from important others regarding whether they should perform a

particular behaviour. In financial contexts, subjective norms arise when

individuals believe that people around them support, encourage, or expect them

to engage in investment-related behaviour. Social factors and subjective norms

are closely connected because continuous exposure to family views, peer

discussions, media narratives, and online financial communities can gradually

build a sense that investment is socially desirable or acceptable. The

literature supports this relationship. Singh et

al. (2025) emphasized that attitudinal and normative

elements play an important role in investor intention, especially when

financial actions are socially discussed and interpreted. Thanki

et al. (2025) also found that the theory of planned behavior, including subjective

norms, remains useful in explaining financial behavioural intention in

investment contexts. Natalia

and Sihombing (2025) further showed that subjective norms are

associated with investment intention and can develop through information

cascades and social influence. This means that when investors are regularly

exposed to investment-related advice and communication, they may develop

stronger normative beliefs about participating in financial markets. Therefore,

social factors are expected to positively influence subjective norms in the

present study.

H2: Social

factors have a significant positive effect on subjective norms.

Subjective Norms and Investment Decision-Making

Subjective norms

influence behaviour by affecting how individuals respond to perceived approval

or expectations from important others. In the case of investment

decision-making, subjective norms may shape whether an individual feels

encouraged to invest, whether investment is viewed as a socially appropriate

action, and whether support from others strengthens decision confidence. This

is especially relevant in uncertain financial contexts, where social

reassurance can reduce hesitation and increase willingness to act. Several

studies support the role of subjective norms in financial and investment

behaviour. Ikhsan

and Wulandari (2024), reported that subjective norms significantly

influence intention to invest, suggesting that social approval remains

important even when investment decisions are framed in formal financial

settings. Rahmayanti

et al. (2025) found that subjective norms help drive

students’ intention to begin stock investing, while Natalia

and Sihombing (2025) also linked subjective norms with investment

intention in a broader behavioral model. Thanki

et al. (2025) similarly supported the importance of subjective norms in mutual fund

investment behaviour. These findings show that individuals often respond not

only to personal reasoning but also to the belief that investment is valued or

approved by others. Thus, subjective norms are expected to positively influence

investment decision-making in the present study.

H3: Subjective

norms have a significant positive effect on investment decision-making.

Comparative Analysis of Gen Z and Millennials

Comparative

analysis in behavioral finance is important when a study includes different

age-based cohorts because generational groups may differ in exposure, financial

experience, social interaction, and decision context. In the present study, Gen

Z and Millennials are compared because both groups are active in modern

financial environments, yet they differ in life stage, digital exposure, and

practical financial responsibility. Gen Z is more likely to be influenced by

rapidly changing online content, peer-led narratives, and early-stage financial

experimentation, whereas Millennials may approach investment with relatively

greater maturity, income experience, and long-term planning. Previous studies

suggest that both generations are important in the study of modern investment

behaviour. Kurniadi

and Herdinata (2024) examined investment decisions among

Millennials and Gen Z and showed that both groups are shaped by behavioural and

financial determinants. Shahzad

et al. (2024) also demonstrated the value of multigroup

analysis in testing whether financial behaviour models differ across categories

of investors. Although it is possible that social factors and subjective norms

may vary slightly in strength across age groups, the broader theoretical

expectation remains that both generations are influenced by comparable

behavioral mechanisms in investment decision-making. Therefore, the present

study tests whether the structural relationships differ significantly between

Gen Z and Millennials.

H4: There is a

significant difference between Gen Z and Millennials in the relationships among

social factors, subjective norms, and investment decision-making.

Conceptual Support for the Study

|

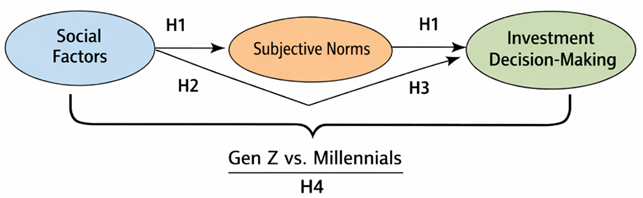

Figure 1 |

|

Figure 1 Conceptual

Framework |

The literature

reviewed above shows that investment decision-making is not merely a rational

economic process but also a socially influenced behaviour. Social factors

provide information, encouragement, and environmental cues, while subjective

norms convert broader social influence into perceived approval or pressure.

Together, these variables create a behavioral pathway through which individuals

form and act on investment decisions. The reviewed studies support the argument

that family influence, peer guidance, digital information exposure, and

normative beliefs all contribute to financial action in meaningful ways Alshebami

and Aldhyani (2022), Ikhsan

and Wulandari (2024), Natalia

and Sihombing (2025), Singh et

al. (2025), Thanki

et al. (2025). Thus, the present study uses these constructs to explain investment

decision-making among Gen Z and Millennials and to compare whether the same

model behaves differently across the two groups.

Research Methodology

Research Design

The present study

adopted a quantitative, descriptive, and comparative research design to examine

the influence of social factors and subjective norms on investment

decision-making among Gen Z and Millennial respondents. The study used a

survey-based approach because it was suitable for collecting measurable

responses and testing the proposed relationships in an empirical manner.

Population and Sample

The target

population of the study comprised individuals belonging to Generation Z (14–29

years) and Millennials (30–45 years). A total of 480 valid responses were

included in the final analysis. The sample covered respondents from different

gender, income, and occupational groups, which made the dataset diverse and

appropriate for comparative generational analysis.

Data Collection

The study was

based on primary data collected through a structured questionnaire. The

questionnaire was prepared in a simple and clear format so that respondents

from both generations could understand the statements and provide suitable

responses.

Measurement of Variables

The questionnaire

measured the main constructs of the study, namely Financial Literacy (FL),

Social Factors (SF), Perceived Behavioral Control (PBC), Subjective Norms (SN),

and Investment Decision-Making (IDM). Most of the items were measured on a

five-point Likert scale, while the items related to subjective norms were

measured on a three-point scale. In this paper, the major emphasis was placed

on social factors and subjective norms as the key variables influencing

investment decision-making.

Tools of Analysis

The collected data

were coded and analyzed using SPSS and Smart PLS 4. SPSS was used for

demographic analysis and descriptive statistics, while Smart PLS 4 was used for

structural model assessment and hypothesis testing.

Structural and Comparative Analysis

The study used

path analysis, mediation analysis, and multi-group analysis (MGA) through Smart

PLS 4. Separate subgroup analysis was conducted for Gen Z and Millennial

respondents in order to compare the structural relationships across the two

generations. The multigroup analysis was applied to determine whether the

differences in the path relationships between the two groups were statistically

significant.

Basis of Hypothesis Testing

The hypotheses

were tested on the basis of path coefficients, standard deviation,

t-statistics, p-values, and coefficient of determination (R²). Significant

paths were accepted, while insignificant paths were rejected according to the

statistical results.

Ethical Considerations

The study was

conducted purely for academic purposes. Participation was voluntary, and the

confidentiality of respondents was maintained throughout the research process.

No personal identity of any respondent was disclosed in the study.

Data Analysis and Results

Demographic Profile

|

Table 1 |

|

Table 1 Demographic

Profile of Respondents (N = 480) |

|||

|

Variable |

Category |

Frequency |

Percent |

|

Gender |

Male |

233 |

48.5 |

|

Female |

247 |

51.5 |

|

|

Age

Group |

14–29

years (Gen Z) |

270 |

56.3 |

|

30–45

years (Millennials) |

210 |

43.8 |

|

|

Income |

Low

Income |

186 |

38.8 |

|

Middle

Income |

156 |

32.5 |

|

|

High

Income |

138 |

28.7 |

|

|

Occupation |

Student |

114 |

23.8 |

|

Private

Job |

129 |

26.9 |

|

|

Self-Employed |

129 |

26.9 |

|

|

Unemployed |

108 |

22.5 |

|

|

Source: Primary

Data Compiled by the Researcher |

|||

The study is based

on 480 respondents. Female respondents (51.5%) are slightly higher than male

respondents (48.5%). In terms of age, 56.3% belong to Gen Z and 43.8% belong to

the Millennial group. Regarding income, 38.8% fall in the low-income category,

32.5% in the middle-income category, and 28.7% in the high-income category. The

occupational profile shows a balanced spread, with 23.8% students, 26.9%

private employees, 26.9% self-employed respondents, and 22.5% unemployed

respondents. This demographic composition indicates that the sample is

adequately diverse and suitable for studying investment decision-making among

Gen Z and Millennials.

|

Table 2 |

|

Table 2 Descriptive Statistics |

|||||

|

N |

Minimum |

Maximum |

Mean |

Std.

Deviation |

|

|

FL1 |

480 |

1.00 |

5.00 |

3.5000 |

.78344 |

|

FL2 |

480 |

1.00 |

5.00 |

3.4833 |

.77523 |

|

FL3 |

480 |

1.00 |

5.00 |

3.4938 |

.78075 |

|

FL4 |

480 |

1.00 |

5.00 |

3.4687 |

.80646 |

|

SF1 |

480 |

1.00 |

5.00 |

3.3021 |

.79034 |

|

SF2 |

480 |

1.00 |

5.00 |

3.3417 |

.78340 |

|

SF3 |

480 |

1.00 |

5.00 |

3.3083 |

.78126 |

|

SF4 |

480 |

1.00 |

5.00 |

3.3063 |

.81987 |

|

PBC1 |

480 |

1.00 |

5.00 |

2.7750 |

.79363 |

|

PBC2 |

480 |

1.00

|

5.00 |

2.7750 |

.75867 |

|

PBC3 |

480 |

1.00 |

5.00 |

2.7688 |

.82918 |

|

SN1 |

480 |

1.00 |

3.00 |

1.4479 |

.54962 |

|

SN2 |

480 |

1.00 |

3.00 |

1.4479 |

.56461 |

|

SN3 |

480 |

1.00 |

3.00 |

1.4750 |

.57741 |

|

IDM1 |

480 |

2.00 |

5.00 |

3.8792 |

.82875 |

|

IDM2 |

480 |

2.00 |

5.00 |

3.8688 |

.82590 |

|

IDM3 |

480 |

2.00 |

5.00 |

3.8854 |

.82333 |

|

IDM4 |

480 |

1.00 |

5.00 |

3.8625 |

.82615 |

|

IDM5 |

480 |

1.00 |

5.00 |

3.9000 |

.83404 |

|

Valid

N (listwise) |

480 |

||||

|

Source: SPSS Output

Based on Primary Data. |

|||||

Table 2 indicates that the items measuring Financial

Literacy have mean values ranging from 3.4687 to 3.5000, suggesting that

respondents generally possess a moderate level of financial awareness and

investment-related understanding. Among these items, FL1 records the highest

mean value of 3.5000, indicating that respondents tend to believe that they

have a reasonably good understanding of investment. The standard deviations for

these items remain below 1.00, which implies a moderate but acceptable spread

of responses. The Social Factors items show mean values between 3.3021 and

3.3417. These values indicate that respondents moderately rely on internet

sources, media information, family, friends, and experts while making

investment decisions. Among the Social Factors items, SF2 reports the highest

mean, suggesting that internet and media-based financial information have a

relatively strong influence on respondents’ investment thinking. The findings

reflect the growing importance of digital information channels in financial

decision-making among younger and middle-aged investors. The Perceived

Behavioral Control items record noticeably lower mean scores, ranging from

2.7688 to 2.7750. This suggests that although respondents may have some

financial awareness, they are comparatively less confident about their

practical ability to identify profitable investments or act quickly in

stock-market settings. In other words, knowledge and confidence do not appear

to move at the same intensity, which strengthens the importance of including

Perceived Behavioral Control as a mediating construct in the model. The

Subjective Norms items register the lowest mean values, between 1.4479 and

1.4750, on a three-point response range. These values suggest that respondents

are relatively less driven by social pressure or social approval when thinking

about stock market participation. However, since the standard deviations remain

low, the responses are fairly consistent. In contrast, the Investment

Decision-Making items produce high mean values ranging from 3.8625 to 3.9000,

indicating that respondents tend to compare investment options, seek advice,

set goals, and consider both risk and return in a systematic manner. This

pattern suggests that the sample demonstrates a relatively rational and deliberate

orientation toward investment behavior.

Structural Model Results for Millennials

The Millennial

subgroup results also support most of the proposed structural relationships and

broadly mirror the pattern observed in the overall sample and Gen Z subgroup.

Financial Literacy significantly affects both Investment Decision-Making and

Perceived Behavioral Control, confirming that financial knowledge remains a

major driver of rational investment behaviour and confidence in financial

action among Millennials. However, just as in the overall model and the Gen Z

analysis, Financial Literacy does not significantly influence Subjective Norms,

which suggests that knowledge alone does not create social approval or

normative pressure for investment participation. Perceived Behavioral Control

significantly affects Investment Decision-Making, demonstrating that

Millennials, like Gen Z respondents, are more likely to make favorable

investment decisions when they feel capable of managing financial options and

uncertainty. Social Factors significantly influence Investment Decision-Making,

Perceived Behavioral Control, and Subjective Norms, while Subjective Norms also

significantly influence Investment Decision-Making. This indicates that

Millennial respondents are also meaningfully shaped by external information,

social surroundings, and normative expectations. The Millennial structural

pattern therefore confirms the continuing importance of financial literacy,

confidence, and social influence in explaining investment decisions within this

generation.

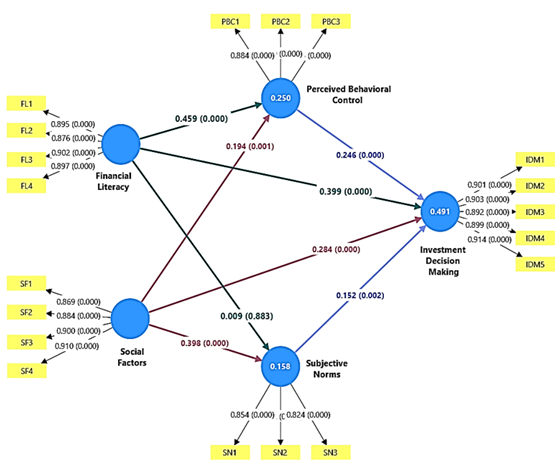

|

Figure 2 |

|

Figure 2 Structural Model

of Investment Decision Making for Millennials (Source: Smart PLS 4 software) |

|

Table 3 |

|

Table 3 Path Analysis and

Hypothesis Testing of Millennials |

|||||

|

Relationship |

Original

Sample (O) |

STDEV |

T

Statistics |

P

Value |

Decision |

|

Financial

Literacy → Investment Decision-Making |

0.399 |

0.056 |

7.077 |

0.000 |

H1b

Supported |

|

Financial

Literacy → Perceived Behavioral Control |

0.459 |

0.049 |

9.378 |

0.000 |

H2b

Supported |

|

Financial

Literacy → Subjective Norms |

0.009 |

0.064 |

0.147 |

0.883 |

H3b

Not Supported |

|

Perceived

Behavioral Control → Investment Decision-Making |

0.246 |

0.056 |

4.384 |

0.000 |

H4b

Supported |

|

Social

Factors → Investment Decision-Making |

0.284 |

0.054 |

5.223 |

0.000 |

H5b

Supported |

|

Social

Factors → Perceived Behavioral Control |

0.194 |

0.060 |

3.242 |

0.001 |

H6b

Supported |

|

Social

Factors → Subjective Norms |

0.398 |

0.056 |

7.095 |

0.000 |

H7b

Supported |

|

Subjective

Norms → Investment Decision-Making |

0.152 |

0.050 |

3.036 |

0.002 |

H8b

Supported |

|

Source: Smart PLS subgroup analysis for

Millennials. |

|||||

The Millennial

subgroup results also support most of the proposed relationships. Financial

Literacy significantly influences Investment Decision-Making (β = 0.399, p

= 0.000) and Perceived Behavioral Control (β = 0.459, p = 0.000), thereby

supporting H1b and H2b. However, just as in the overall sample and the Gen Z

subgroup, Financial Literacy does not significantly affect Subjective Norms

(β = 0.009, p = 0.883), leading to rejection of H3b. Perceived Behavioral

Control significantly affects Investment Decision-Making (β = 0.246, p =

0.000), supporting H4b. Social Factors exert significant positive effects on

Investment Decision-Making, Perceived Behavioral Control, and Subjective Norms,

supporting H5b, H6b, and H7b. Subjective Norms also significantly influence

Investment Decision-Making (β = 0.152, p = 0.002), which supports H8b. The

Millennial pattern therefore mirrors the broader logic of the model, with

Financial Literacy and Social Factors emerging as important drivers of

investment outcomes.

|

Table 4 |

|

Table 4 Mediating |

|||||

|

Relationship |

Original

Sample (O) |

STDEV |

T

Statistics |

P

Value |

Decision |

|

Social

Factors → Perceived Behavioral Control → Investment

Decision-Making |

0.048 |

0.018 |

2.597 |

0.009 |

H11b

Supported |

|

Financial

Literacy → Subjective Norms → Investment Decision-Making |

0.001 |

0.010 |

0.138 |

0.890 |

H10b

Not Supported |

|

Financial

Literacy → Perceived Behavioral Control → Investment

Decision-Making |

0.113 |

0.030 |

3.780 |

0.000 |

H9b

Supported |

|

Social

Factors → Subjective Norms → Investment Decision-Making |

0.060 |

0.021 |

2.859 |

0.004 |

H12b

Supported |

|

Source: Smart PLS subgroup mediation

output for Millennials. |

|||||

For Millennials,

Perceived Behavioral Control significantly mediates the relationship between

Financial Literacy and Investment Decision-Making (β = 0.113, p = 0.000),

which supports H9b. Social Factors also affect Investment Decision-Making

indirectly through Perceived Behavioral Control (β = 0.048, p = 0.009),

supporting H11b, and through Subjective Norms (β = 0.060, p = 0.004),

supporting H12b. As in the Gen Z subgroup, Subjective Norms do not mediate the

relationship between Financial Literacy and Investment Decision-Making (β

= 0.001, p = 0.890), and thus H10b is not supported. The mediation pattern for

Millennials therefore confirms that knowledge primarily works through

capability, while social influences operate through both confidence and

normative pathways.

|

Table 5 |

|

Table 5 Coefficient of

Determination (R²) |

||

|

Construct |

R² |

Adjusted

R² |

|

Investment

Decision-Making (IDM) |

0.491 |

0.487 |

|

Perceived

Behavioral Control (PBC) |

0.25 |

0.246 |

|

Subjective

Norms (SN) |

0.158 |

0.154 |

|

Source:

SmartPLS subgroup analysis for Millennials. |

||

The Millennial

subgroup explains 49.1 percent of the variance in Investment Decision-Making,

25.0 percent of the variance in Perceived Behavioral Control, and 15.8 percent

of the variance in Subjective Norms. These values are slightly lower for

Investment Decision-Making and Perceived Behavioral Control than those reported

for Gen Z, but slightly higher for Subjective Norms. This suggests that while

the model fits both generations well, normative influence may be marginally

more stable among Millennials than among Gen Z respondents.

Multi-Group Analysis (MGA)

The multigroup

analysis was conducted to test whether the structural relationships among the

study variables differ significantly between Gen Z and Millennials. This is an

important final analytical step because the study does not merely seek to

identify significant paths within each group but also to determine whether the

overall model functions differently across generational categories. The results

show that none of the structural path differences between Gen Z and Millennials

are statistically significant at the conventional level. Although some

individual coefficients differ slightly in magnitude, these differences are not

large enough to indicate a meaningful structural distinction between the two

groups. This finding leads to rejection of the multigroup difference hypothesis

and suggests that the conceptual model operates in a broadly similar manner for

both Gen Z and Millennial respondents. In substantive terms, this means that

the effects of Financial Literacy, Social Factors, Perceived Behavioral Control,

and Subjective Norms on Investment Decision-Making are not generation-specific

in the present sample. This is a notable finding because it indicates a shared

pattern of investment behavior across the two cohorts, despite their different

age positions and social experiences.

|

Table 6 |

|

Table 6 Multigroup Analysis |

||||

|

Relationship |

Difference

(Gen Z – Millennials) |

1-tailed

p value |

2-tailed

p value |

Decision |

|

Financial

Literacy → Investment Decision-Making |

-0.059 |

0.790 |

0.420 |

Not

Significant |

|

Financial

Literacy → Perceived Behavioral Control |

0.022 |

0.371 |

0.742 |

Not

Significant |

|

Financial

Literacy → Subjective Norms |

-0.006 |

0.529 |

0.942 |

Not

Significant |

|

Perceived

Behavioral Control → Investment Decision-Making |

0.051 |

0.246 |

0.492 |

Not

Significant |

|

Social

Factors → Investment Decision-Making |

0.024 |

0.365 |

0.730 |

Not

Significant |

|

Social

Factors → Perceived Behavioral Control |

0.094 |

0.110 |

0.221 |

Not

Significant |

|

Social

Factors → Subjective Norms |

-0.030 |

0.655 |

0.689 |

Not

Significant |

|

Subjective

Norms → Investment Decision-Making |

0.046 |

0.244 |

0.489 |

Not

Significant |

|

Source: Smart PLS multigroup analysis output. |

||||

Table 6 clearly shows that none of the two-tailed

p-values is below 0.05. Therefore, there is no statistically significant

difference in any of the structural paths between Gen Z and Millennial

respondents. On this basis, H13 is not supported. The absence of significant

difference indicates that the proposed model functions in a broadly similar way

across both generational groups. This is an important finding because it

suggests that the effects of Financial Literacy, Social Factors, Perceived

Behavioral Control, and Subjective Norms on Investment Decision-Making are not

generation-specific within the present sample. Although the path coefficients

differ slightly in magnitude, those differences are not strong enough to be

considered statistically meaningful. Hence, the study concludes that Gen Z and

Millennials exhibit a comparable investment decision-making pattern under the

conceptual model used in this research.

Discussion

The findings of

the present study confirm that social factors and subjective norms play a

meaningful role in shaping investment decision-making among Gen Z and

Millennial respondents. The significant positive effect of social factors on

investment decision-making suggests that individuals do not make financial

choices in isolation; rather, their decisions are influenced by family views,

peer discussions, media exposure, internet-based financial information, and

expert guidance. This result supports the broader behavioral finance

literature, which argues that financial behaviour is often socially embedded

and affected by the surrounding information environment Alshebami

and Aldhyani (2022), Ammar et

al. (2025),Tabassum et al. (2021).

In practical terms, the result indicates that respondents use social and

informational cues to interpret investment opportunities, reduce uncertainty,

and strengthen their decision process. This pattern is especially relevant in

modern digital settings where investment ideas circulate rapidly through online

communities and media channels. The

study also finds that social factors significantly influence subjective norms,

which means that continued exposure to social and informational environments

contributes to the development of perceived social approval regarding

investment participation. This result is theoretically consistent with the view

that subjective norms are not formed independently but emerge through

communication, shared beliefs, and repeated contact with social expectations.

When individuals are frequently exposed to supportive investment-related

messages from peers, families, and financial communities, they are more likely

to feel that investment is a socially acceptable and desirable activity. This

finding is in line with prior studies that emphasize the role of normative and

social influences in financial intention and investment-related behavior Natalia

and Sihombing (2025), Singh et

al. (2025), Thanki

et al. (2025). It also confirms that subjective norms remain relevant in

contemporary financial decision-making, even in situations where individuals

have access to independent information.

Another important

finding of the study is that subjective norms significantly influence

investment decision-making in both generations. This suggests that perceived

approval, encouragement, and social expectation contribute positively to actual

investment behaviour. Individuals appear more likely to make investment

decisions when they believe that important others view such behaviour

positively. This result is consistent with theory-based investment studies that

identify subjective norms as a key behavioral determinant, particularly in

contexts where people seek reassurance before committing to uncertain financial

actions Ikhsan

and Wulandari (2024), Rahmayanti

et al. (2025), Thanki

et al. (2025). The result also supports the argument that investment behaviour is

not purely rational or individualistic; instead, it is partly shaped by how

people interpret the expectations and support of those around them. In this

sense, subjective norms function as a social-psychological mechanism through

which broader social influence affects actual financial action. The Millennial subgroup results further

deepen the interpretation of the model. For Millennials, social factors

significantly influenced investment decision-making, perceived behavioral

control, and subjective norms, while subjective norms also significantly

influenced investment decision-making. This indicates that Millennials are

shaped not only by financial literacy and internal confidence but also by

external information and social surroundings. The significant indirect effects

of social factors through both perceived behavioral control and subjective

norms show that social influence works through multiple channels. On one hand,

it strengthens confidence and perceived ability; on the other hand, it creates

a sense of social legitimacy around investment activity. This pattern is

consistent with earlier research highlighting the interaction of literacy,

behavioral capability, and external influence in financial decision-making Jain et al. (2023), Kumar et

al. (2023), Shahzad

et al. (2024). It also suggests that Millennials respond

to social influence in a fairly structured way, where external cues contribute

to both internal readiness and socially guided decision behaviour.

The study also

provides an important comparative insight through the multigroup analysis,

which shows that none of the structural path differences between Gen Z and

Millennials are statistically significant. Although the coefficients differ

slightly in magnitude, the differences are not strong enough to suggest that

the model operates differently across the two generations. This is a notable

finding because it indicates that the influence of social factors and

subjective norms on investment decision-making is broadly similar across both

cohorts. Earlier research often suggests that Gen Z may be more socially

reactive because of stronger digital exposure, while Millennials may behave

more independently because of greater life-stage maturity. However, the present

findings show that both groups follow a comparable investment decision pattern

under the proposed conceptual framework. This result supports the multigroup

logic highlighted in comparative financial behavior studies and suggests that

socially shaped investment behaviour may be more stable across adjacent

generations than commonly assumed Kurniadi

and Herdinata (2024), Shahzad

et al. (2024). At

the same time, the findings should also be interpreted alongside the broader

model in which financial literacy and perceived behavioral control remain

important. While this paper emphasizes social factors and subjective norms, the

results indicate that investment behaviour is best understood as the outcome of

an interaction between financial understanding, internal capability, and social

influence. Earlier studies have similarly shown that financial decision-making

becomes stronger when knowledge, behavioral confidence, and social context are

considered together rather than separately Adil et al. (2022), Ahmad

and Shah (2022), Hussain

et al. (2022), Suresh

(2024). Therefore, the present discussion suggests

that social factors and subjective norms should not be treated as secondary

influences; instead, they should be viewed as integral elements of the

investment decision environment for both Gen Z and Millennials.

Conclusion and Implications

The present study

concludes that social factors and subjective norms are significant determinants

of investment decision-making among Gen Z and Millennial respondents. The

findings show that investment decisions are influenced not only by individual

reasoning and financial understanding but also by family views, peer

discussions, media exposure, internet-based financial information, and

perceived social approval. The significant positive effect of social factors on

investment decision-making indicates that respondents meaningfully rely on

their surrounding information and social environment when making financial

choices, while the significant influence of subjective norms confirms that

encouragement, support, and approval from important others contribute positively

to investment behaviour. The study further concludes that these influences

operate in a broadly similar manner across both generations, as the multigroup

analysis shows no statistically significant difference in the structural

relationships between Gen Z and Millennials. This suggests that socially

influenced investment behaviour is not confined to one generation but remains

relevant across both younger and middle-aged investor groups. Overall, the

study establishes that investment decision-making is a socially embedded

process in which external influence and normative expectations play an

important role alongside personal and behavioral factors.

Implications

·

For

policymakers: Financial

awareness programs should include social and community influence, not only

individual literacy.

·

For

educators: Investment

education should teach students how to assess peer advice, media content, and

online financial information critically.

·

For

financial service providers: Platforms

should provide credible, simple, and responsible financial communication for

both Gen Z and Millennials.

·

For

families and social groups:

Positive and informed discussion about investment can support better financial

decision-making.

·

For

researchers: Future studies

can test the same model in other age groups, regions, or financial contexts.

ACKNOWLEDGMENTS

None.

REFERENCES

Adil, M., Singh, Y., and Ansari, M. S. (2022). How Financial Literacy Moderates the Association Between Behaviour Biases and Investment Decision? Asian Journal of Accounting Research, 7(1), 17–30. https://doi.org/10.1108/AJAR-09-2020-0086

Ahmad, M., and Shah, S. Z. A. (2022). Overconfidence Heuristic-Driven Bias in Investment Decision-Making and Performance: Mediating Effects of Risk Perception and Moderating Effects of Financial Literacy. Journal of Economic and Administrative Sciences, 38(1), 60–90. https://doi.org/10.1108/JEAS-07-2020-0116

Alshebami, A. S., and Aldhyani, T. H. (2022). The Interplay of Social Influence, Financial Literacy, and Saving Behaviour Among Saudi Youth and the Moderating Effect of Self-Control. Sustainability, 14(14), Article 8780. https://doi.org/10.3390/su14148780

Ammar, M., Ali, A., and Audi, M. (2025). The Impact of Financial Literacy on Investment Decisions: The Mediating Role of Peer Influence and the Moderating Role of Financial Status. Journal for Current Sign, 3(2), 379–411.

Arora, J., and Chakraborty, M. (2023). Role of Financial Literacy in Investment Choices of Financial Consumers: An Insight from India. International Journal of Social Economics, 50(3), 377–397. https://doi.org/10.1108/IJSE-12-2021-0764

Atkinson, A., and Messy, F. A. (2012). Measuring Financial Literacy. OECD Working Papers on Finance, Insurance and Private Pensions (No. 15). OECD Publishing. https://doi.org/10.1787/5k9csfs90fr4-en

Biswas, S., and Gupta, A. (2021). Impact of Financial Literacy on Household Decision-Making: A Study in the State of West Bengal in India. International Journal of Economics and Financial Issues, 11(5), 104–110. https://doi.org/10.32479/ijefi.11759

Gupta, N., Rana, R., and Tandon, D. (2025). Financial Literacy as a Moderator in Behavioral Biases and Investor Decisions. Indian Journal of Finance, 19(5), 79–94. https://doi.org/10.17010/ijf/2025/v19i5/175045

Hussain, A., Kijkasiwat, P., Rehman, H. U., and Ullah, M. Z. (2022). Financial Literacy and Investment Decisions: Evidence from Pakistan. South Asian Journal of Finance, 2(2). https://doi.org/10.4038/sajf.v2i2.46

Ikhsan, M. A., and Wulandari, R. (2024). Impact of Attitude, Subjective Norms, and Perceived Behavioural Control on Intention to Invest in Retail Green Sukuk Among Muslim Millennials in Jabodetabek. Journal of Islamic Economics Lariba, 10(1), 149–168. https://doi.org/10.20885/jielariba.vol10.iss1.art9

Iram, T., Bilal, A. R., and Ahmad, Z. (2023). Investigating the Mediating Role of Financial Literacy on the Relationship Between Women Entrepreneurs' Behavioral Biases and Investment Decision Making. Gadjah Mada International Journal of Business, 25(1), 93–118. https://doi.org/10.22146/gamaijb.65457

Iram, T., Iqbal, N., Qazi, R., and Saleem, S. (2021). Nexus Between Financial Literacy, Investment Decisions and Heuristic Biases of Women Entrepreneurs: A Way Forward for Women Empowerment. Pakistan Journal of Social Sciences, 41(1), 221–234.

Jain, R., Sharma, D., Behl, A., and Tiwari, A. K. (2023). Investor Personality as a Predictor of Investment Intention: Mediating Role of Overconfidence Bias and Financial Literacy. International Journal of Emerging Markets, 18(12), 5680–5706. https://doi.org/10.1108/IJOEM-12-2021-1885

Kanagasabai, B., and Aggarwal, V. (2020). The Mediating Role of Risk Tolerance in the Relationship Between Financial Literacy and Investment Performance. Colombo Business Journal, 11(1), 83–100. https://doi.org/10.4038/cbj.v11i1.58

Kumar, P., Pillai, R., Kumar, N., and TaBash, M. I. (2023). The Interplay of Skills, Digital Financial Literacy, Capability, and Autonomy in Financial Decision Making and Well-Being. Borsa Istanbul Review, 23(1), 169–183. https://doi.org/10.1016/j.bir.2022.09.012

Kurniadi, A. C., and Herdinata, C. (2024). Factors Affecting Investment Decisions on Millennials and Gen Z. Jurnal Manajemen, 28(3), 477–494. https://doi.org/10.24912/jm.v28i3.2008

Nag, A. K., and Shah, J. (2022). An Empirical Study on the Impact of Gen Z Investors' Financial Literacy to Invest in the Indian Stock Market. Indian Journal of Finance, 16(10), 43–59. https://doi.org/10.17010/ijf/2022/v16i10/172387

Natalia, E., and Sihombing, S. O. (2025). Attitude, Subjective Norm, Perceived Behavioral Control, and Information Cascade Effects on Investment Intention: Financial literacy as Antecedent to Attitude. DeReMa (Development Research of Management): Jurnal Manajemen, 20(2). https://doi.org/10.19166/derema.v20i2.10042

Prasad, S., Kiran, R., and Sharma, R. K. (2021). Behavioural, Socio-Economic Factors, Financial Literacy and Investment Decisions: Are Men More Rational and Women More Emotional? The Indian Economic Journal, 69(1), 66–87. https://doi.org/10.1177/0019466220987023

Rahmayanti, P. L. D., Sasrawan, I. P. H., and Yasa, N. N. K. (2025). Decoding Investment Intentions: Uncovering How Risk Tolerance, Financial Literacy, and Subjective Norms Drive Students to Begin Stock Investing. Asian Journal of Economics, Business and Accounting, 25(2), 157–166. https://doi.org/10.9734/ajeba/2025/v25i21671

Ranaweera, S. S., and Kawshala, B. A. H. (2022). Influence of Behavioral Biases on Investment Decision Making with Moderating Role of Financial Literacy and Risk Attitude: A Study Based on Colombo Stock Exchange. South Asian Journal of Finance, 2(1). https://doi.org/10.4038/sajf.v2i1.32

Rani, M., and Siwach, M. (2023). Financial Literacy in India: A Review of Literature. Economic and Regional Studies, 16(3), 446–458. https://doi.org/10.2478/ers-2023-0029

Raut, R. K. (2020). Past Behaviour, Financial Literacy and Investment Decision-Making Process of Individual Investors. International Journal of Emerging Markets, 15(6), 1243–1263. https://doi.org/10.1108/IJOEM-07-2018-0379

Sari, M. (2025). Exploring the Roles of Financial Literacy, Past Behavior, and Subjective Norms in Shaping Investment Intention: A Mediation Analysis. Investment Management and Financial Innovations, 22(4), Article 30. https://doi.org/10.21511/imfi.22(4).2025.03

Shahzad, M. A., Jianguo, D., Jan, N., and Rasool, Y. (2024). Perceived Behavioral Factors and Individual Investor Stock Market Investment Decision: Multigroup Analysis and Major Stock Markets Perspectives. Sage Open, 14(2), 21582440241256210. https://doi.org/10.1177/21582440241256210

Singh, A., Goel, U., Kumar, S., and Johri, A. (2025). Unveiling the Attitudinal Factors: An Integration of TPB and SCT in Understanding Investor Intention Towards Equity Investments. Humanities and Social Sciences Communications, 12(1), 1–14. https://doi.org/10.1057/s41599-025-05478-4

Song, C. L., Pan, D., Ayub, A., and Cai, B. (2023). The Interplay Between Financial Literacy, Financial Risk Tolerance, and Financial Behaviour: The Moderator Effect of Emotional Intelligence. Psychology Research and Behavior Management, 16, 535–548. https://doi.org/10.2147/PRBM.S398450

Subramanian, R., and Arjun, T. P. (2024). Do Explicit and Implicit Parental Financial Socialization Influence Students' Financial Literacy? Evidence from India. Indian Journal of Finance, 18(10), 24–39. https://doi.org/10.17010/ijf/2024/v18i10/174612

Suresh, G. (2024). Impact of Financial Literacy and Behavioural Biases on Investment Decision-Making. FIIB Business Review, 13(1), 72–86. https://doi.org/10.1177/23197145211035481

Thanki, H., Tripathy, N., and Shah, S. (2025). Investors' Behavioral Intention in Mutual Fund Investments in India: Applicability of Theory of Planned Behavior. Asia-Pacific Financial Markets, 32(3), 975–996. https://doi.org/10.1007/s10690-024-09477-4

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© ShodhPrabandhan 2026. All Rights Reserved.