|

|

|

|

Original Article

DOES INCREASE IN TAX LIMIT IMPACT INVESTMENT BEHAVIOR OF WOMEN SALARIED INVESTORS WITH REFERENCE TO HIGHER SECONDARY TEACHERS

|

Dr. Renati Jayaprakash Reddy 1* 1 Professor, Department of

Commerce, Acharya Institute of Management and Sciences, Bangalore, India 2 Research Scholar, AIMS Centre for

Advanced Research Centre, University of Mysore, Mysore,

Karnataka, India |

|

|

|

ABSTRACT |

||

|

Tax policy reforms play an important role in influencing the saving and investment behaviour of salaried individuals. This study aims to examine the impact of the revised tax exemption limit on fund utilization and investment behaviour of women salaried employees. The study is based on primary data collected from 538 higher secondary women teachers working in Bengaluru and Tumkur districts using a structured questionnaire. Reliability analysis confirmed the internal consistency of the instrument with a Cronbach’s alpha value above 0.8. The findings indicate that the earlier tax regime encouraged disciplined savings through investments in instruments such as Public Provident Fund (PPF), Life Insurance policies, National Savings Certificates, pension schemes, and tax-saving fixed deposits, offering returns between 7% and 15%. However, the removal of deduction-based incentives under the new tax regime has reduced the compulsion to save, resulting in a shift toward increased consumption and leisure spending. Although investments in mutual funds and the stock market remain preferred avenues, the overall tendency for tax-driven savings has declined. The study concludes that while the new regime enhances disposable income and simplifies taxation, it may weaken long-term investment behaviour unless supported by stronger financial awareness and planning initiatives. Keywords: Tax Exemption Limit, Investment Behaviour, Women Salaried Investors, Tax Regime Reform,

Financial Savings and Investment |

||

INTRODUCTION

An integral component of a nation's financial system is income tax. It assists the government in raising funds for critical public services like social welfare, infrastructure, healthcare, and education. Since this tax is levied directly on both individual and corporate income, it guarantees that everyone makes a contribution to the development of the nation regardless of their income level. The Income Tax Act, 1961, governs income taxation in India. The system is progressive, meaning that those with higher incomes pay a larger proportion of taxes. A person's age, income level, and tax regime preference all affect the tax rates. Tax planning has become a crucial component of financial management for individual taxpayers, particularly those in the salaried and middle-income segments. By using available deductions under sections like 80C, 80D, and 24(b), among others, people seek to legally reduce their tax liability through efficient tax planning. This enables them to set aside money for healthcare, education, retirement savings, insurance, and investments, reaching their financial objectives while adhering to tax regulations.

The Indian government made substantial changes to the income tax system in the Union Budget for 2025, especially with regard to the new tax system. The most significant modification is the raising of the annual income tax exemption threshold to ₹12 lakhs. This implies that people who make up to ₹12 lakhs annually won't have to pay any income tax. Because of a standard deduction of ₹75,000, the exemption limit for salaried individuals is ₹12.75 lakh. The income tax exemption limit has been raised to ₹12 lakhs, which is expected to significantly increase people's disposable income. It is anticipated that many will make responsible and beneficial use of these extra savings. A sizable amount might go toward long-term investments that help people accumulate wealth and safeguard their future, like mutual funds, fixed deposits, or public provident funds (PPF). Others might decide to lower their current debts, such as school or home loans, in order to strengthen their credit and stability. In order to improve their financial readiness for emergencies, more and more people are also using this excess to purchase life and health insurance. In order to improve their career prospects, taxpayers are also investing in professional certifications or online courses as part of a trend toward skill development and education. Many families use their savings to start small businesses, make home improvements, or send their kids to a good school—all of which have a positive impact on the economy as a whole and on individual development. In addition to giving people more power, this prudent use of tax savings boosts the economy by encouraging investment and consumption.

THEORETICAL BACKGROUND

The amount of money set aside for future use rather than being spent on present consumption is referred to as savings. Income levels, consumption habits, financial objectives, and psychological aspects all have an impact on saving. The Life-Cycle Hypothesis Modigliani and Brumberg (1954) states that people's saving behavior at various phases of life is motivated by their desire to balance their consumption throughout the course of their lives. With the goal of producing returns over time, investments entail putting saved funds into tangible or financial assets (such as stocks, bonds, and real estate). Risk tolerance, expectations for the future, financial literacy, and cognitive-emotional aspects all influence investment behavior. By maximizing the ratio of risk to return, Modern Portfolio Theory Markowitz (1952) offers a logical foundation for investing.

Daniel Goleman (1995) defined emotional intelligence (EI) as the capacity to successfully recognize, utilize, comprehend, and control one's own and other people's emotions. EI is made up of five main parts: Self-knowledge, Self-control, Inspiration, Compassion, Social abilities. Decision-making is positively impacted by high EI, especially when there is uncertainty, as in the case of investments and saves. Self-control, for example, can stop rash financial decisions, and emotional intelligence can assist in coordinating expenditures with long-term objectives and beliefs. Financial behaviors are greatly influenced by personality attributes. An established psychological framework is offered by the Five-Factor Model (Big Five), which consists of the following traits: neuroticism, agreeableness, extraversion, conscientiousness, and openness. Disciplined investing and wise saving are correlated with conscientiousness. Impulsive spending and inadequate financial planning are frequently the results of neuroticism. Investment risk-taking may be encouraged by transparency. How people see risk, evaluate future results, and control their emotional reactions to financial stress are all influenced by their personalities.

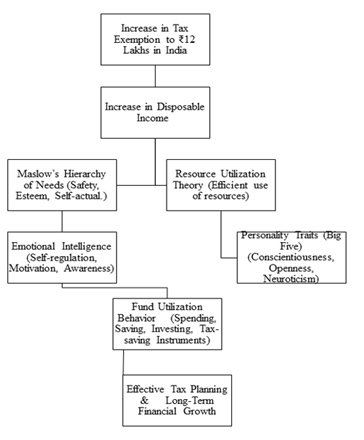

According to resource utilization theory, people may effectively accomplish their goals by managing their internal and external resources, such as time, money, skills, and knowledge. This idea, which has its roots in management and educational theory, holds that optimizing resources enhances individual efficacy and life results. This hypothesis supports how people divide their resources between investing, saving, and consuming in a financial setting. Effective resource management is linked to: Improved budgeting, coping mechanisms that are flexible, thinking strategically and having foresight. Since people must control their internal resources (such as motivation and attention) in order to use external ones successfully, this theory also touches on emotional intelligence and personality. Five levels make up the motivational theory known as Maslow's Hierarchy of Needs (1943): Physiological requirements (water, food) - Needs for safety (financial stability, security) -Love and belonging - Esteem (success, self-respect) - Realization of oneself Generally speaking, investments and savings meet safety needs by providing a feeling of stability and control over unforeseen circumstances. People may invest in long-term development, education, or self-actualization when their fundamental requirements are met. This shows a higher level of financial goal-setting and resource allocation. Taxpayers will be affected behaviourally, emotionally, and psychologically by the proposed tax policy change that would increase the exemption to ₹12 lakhs. In addition to economic issues, psychological factors such as motivational priorities, personality traits, emotional intelligence, and the capacity to make efficient use of available resources all influence how beneficial a change is seen to be. This integrated approach offers a thorough lens through which to examine how Indian taxpayers see, budget, and spend money under a new tax system.

|

Figure 1

|

|

Figure 1 A Model for

Factors Influencing Fund Utilization and Effective Tax Planning for Future

Financial Growth |

REVIEW OF LITERATURE

Theory of investment explained the investment decision as a behavioural response influenced by personality traits and emotional intelligence King et al. (2016).

The respondents in this research is salaried women and hence, the first choice will be risk aversion. At the same time, the inflation effect has to be minimised Peterson et al. (2021).

Under 80C itself there are both volatile and non-volatile investment opportunities. In the portfolio linked and unit linked investment, investment analysis is essential. But the increasing living expenses cause financial constraints Abdeljawad et al. (2023).

Investment behaviour depends on four factors, income, expenditure, financial planning and investment awareness Mastufa Ahmed. (2024).

Future financial planning is the prime part of investment and it is a need based like children education, housing, healthcare, life insurance, saving etc and there are provisions for tax benefit under Income Tax 80C tax exemptions Alfathya et al. (2025).

Investment is always a financial planning and use of fund for a future return in which the priority are given to health care (2025 Global Health Care Outlook), children education (Child-Centred Investments to Achieve Targets of Vision 2025 by Department of Women Development and Child Welfare, Government of Telangana), or in tax saving investments. The Income tax norms have been modified by introducing a set of new norms as the salary income increased. But the investment motivation aroused from the regime 1 was removed from the tax payers as it is not mandatory to do any investment to save tax in regime 2.

RESEARCH GAP

Even though the new tax system (Regime 2) has lower tax rates and easier rules to follow, many workers are still not sure whether to choose the old system (Regime 1) or the new one.

They lose chances to invest their tax savings in high-return options like stocks and bonds because they don't know enough about them. Recently the income tax exemption limit in India has gone up to ₹12 lakhs, people have more money to spend. If they plan their taxes carefully and put that money into investments like mutual funds, retirement plans, and insurance, they can greatly improve their long-term financial security, build wealth, and overall fiscal discipline. This study aims to address this gap and help employees make better tax and investment decisions.

STATEMENT OF THE PROBLEM

Many salaried employees are still unsure about which tax system to choose and how to maximize their tax savings. The Indian government has introduced a new tax system with lower rates and raised the income tax exemption limit to ₹12 lakhs. This aims to increase disposable income and simplify compliance. These people often fail to invest their tax savings in profitable assets like stocks, mutual funds, and retirement plans because they do not have enough financial knowledge or understanding. Their lack of knowledge about tax and investment planning hinders their ability to build wealth and achieve long-term financial security. This also results in missed opportunities for overall economic and financial growth. This study seeks to explore the root causes of this gap to help employees make better decisions in tax and investment planning.

OBJECTIVES OF THE STUDY

· To assess the awareness and understanding of individuals regarding the increased income tax exemption limit.

· To examine how the increase in the income tax exemption limit to ₹12 lakhs influences the fund utilization behaviour of salaried employees in Bangalore.

· To analyse how raised exemption limits influence individuals' tax planning strategies and investment decisions.

RESEARCH METHODOLOGY

The data has been collected using a structured questionnaire from the higher secondary education women teachers in Bengaluru & Tumkur districts. Its Cronbach alpha is more than .8 for all grouped data. Number of samples of the study is 538.

|

Table 1 |

|

Table 1 Demographic Profile of Respondents |

||

|

Variables |

Percent |

|

|

Educational Qualification |

Post Graduation |

28.6 |

|

Doctorate |

71.4 |

|

|

Domain |

Commerce & Management |

12.6 |

|

Art |

7.1 |

|

|

Humanity & Sociology |

39.2 |

|

|

Technological |

20.8 |

|

|

Medical |

20.3 |

|

|

Income |

Rs 40-60K |

11 |

|

Rs. 60-80K |

8.7 |

|

|

Rs. 80-100k |

38.5 |

|

|

Rs 100-120K |

20.1 |

|

|

More than 120K |

21.7 |

|

|

Family Size |

2 |

10.8 |

|

3 |

8.7 |

|

|

4 |

34.4 |

|

|

5 |

24.3 |

|

|

More than 5 |

21.7 |

|

|

Family Structure |

Single |

9.9 |

|

Couple |

9.3 |

|

|

Family |

36.8 |

|

|

Joint Family |

19.1 |

|

|

HUF |

24.9 |

|

|

Awareness on Investment |

Never |

10.8 |

|

basic |

10.2 |

|

|

moderate |

36.8 |

|

|

High |

21.4 |

|

|

Very deep |

20.8 |

|

|

Investments Preferred |

Fixed deposit |

9.3 |

|

SIP |

11.2 |

|

|

Mutual funds |

43.9 |

|

|

Stock market |

18.6 |

|

|

Own Business |

17.1 |

|

|

Information Sources |

Books |

10.2 |

|

Social media |

10.4 |

|

|

Financial Websites |

40.7 |

|

|

Economics Magazines |

17.3 |

|

|

Newspapers |

21.4 |

|

The respondent distribution shows that 71.4% of the respondents are doctorates while 39.2% of the respondents are of humanity & Sociology while technological (20.8%) and medical (20.3%). 80.3% of the respondents are of more than Rs 80K. 19.5% of the respondents have family size less than 3 members and 80.5% of the respondents have more 4 family members.

Single (9.9%) Couple (9.3%) Family (36.8%), Joint Family (19.1%), and HUF (24.9%) are the family members. Family stricture is important in investment decisions, savings and investment decisions.

Never (10.8), basic (10.2), moderate (36.8), High (21.4), Very deep (20.8) are scales in investment awareness. 42.2% of the respondents have a good awareness.

Investments preferred include Fixed deposit (9.3%), SIP (11.2%), Mutual funds (43.9%), Stock market (18.6%), Own Business (17.1%). 43.9% of the respondents prefer mutual funds and 18.6% of the respondents prefer stock market.

Books (10.2%), Social media (10.4%), Financial Websites (40.7%), Economics Magazines (17.3%) Newspapers (21.4%) are the source of information.

The results show that the higher income, large family size, and risk avoidance & financial websites are the main sources for investment decisions.

|

Table 2 |

|

Table 2

Tax Planning in Old Regime of Income Tax |

|||||||

|

Deduction

Type |

Investment |

Yes |

<Rs25K |

25-50K |

50-100K |

100-150K |

Average

return |

|

80C |

Equity

Linked Schemes |

23% |

14% |

9% |

|

|

12-15% |

|

|

PPF |

32% |

11% |

11% |

|

|

7.10% |

|

|

NSC |

23% |

15% |

6% |

3% |

|

7.70% |

|

|

LIC |

62% |

29% |

21% |

12% |

|

8-12% |

|

|

Principal

sum of Home loan |

37% |

13% |

18% |

6% |

|

Nil |

|

80CCC |

Pension funds |

39% |

28% |

8% |

3% |

|

9-12% |

|

80CCD |

Atal

Pension Yojana/ Govt Pension schemes like NOS |

23% |

12% |

9% |

1% |

|

8-10% |

|

Other Schemes in 80C |

Tax saving FD |

42% |

13% |

17% |

9% |

3% |

7-8% |

|

|

Senior

Citizen saving Scheme |

21% |

9% |

7% |

5% |

|

8.20% |

|

|

Sukanya Samriddhi Yojana |

29% |

18% |

9% |

2% |

|

8% |

|

80D |

Health

insurance |

56% |

23% |

21% |

12% |

|

Nil |

The taxable income of salaried individuals under the old income tax regime was determined after deducting the standard deduction and eligible deductions under Sections 80C and 80D. Taxpayers invested in instruments such as PPF, LIC, ELSS, NSC, tax-saving fixed deposits, and health insurance to reduce their taxable income. These investment avenues generally provided average annual returns ranging from 7% to 15%. The applicable tax rates were 5% (₹2.5–5 lakh), 20% (₹5–10 lakh), and 30% (above ₹10 lakh). However, under the new tax regime, most deductions are removed, though a standard deduction of ₹75,000 is allowed and income up to ₹12 lakh effectively attracts no tax due to rebate provisions, which may reduce the motivation for tax-saving investments. From the income information, all the respondents have income tax commitment,

· ₹0 - ₹4 Lakh: Nil

· ₹4,00,001 - ₹8 Lakh: 5%

· ₹8,00,001 - ₹12 Lakh: 10%

· ₹12,00,001 - ₹16 Lakh: 15%

· ₹16,00,001 - ₹20 Lakh: 20%

· ₹20,00,001 - ₹24 Lakh: 25%

· Above ₹24 Lakh: 30%

|

Table 3 |

|

Table 3 Based on

Respondents in This Survey, The Tax Commitment In % |

||

|

Tax slab |

Tax % |

Percentage of respondents

committed |

|

Rs. 4-8L |

5% |

11.0% |

|

Rs. 8-12L |

10% |

47.2% |

|

Rs. 12-16L |

15% |

20.1% |

|

Rs. 100-120L |

20% |

21.7% |

In new regime, there is no deductions but there are more slabs and the tax percentage reduced. The main challenge is in the higher investments by the tax payers to do tax saving and there is financial planning to save tax. Also, these investments cause a saving and investment as a compulsion. But in new regime, as there is no compulsion to save and hence, there is a tendency to spent more. It is a negative effect from the perspective an investor as the saving reduces.

|

Table 4 |

|

Table 4 Investment

Behaviour as There Is No Tax Saving Investments and Lower Scale Taxation |

||

|

Variable |

Mean |

Standard deviation |

|

No saving as there is no 80C

exemptions |

4.32 |

.56 |

|

Leisure |

4.56 |

.43 |

|

Investment on home

appliances |

1,8 |

.45 |

|

Stock market |

2.3 |

.34 |

|

Mutual funds |

2.6 |

.38 |

This shows that the withdrawal of 80C provisions reduced the saving and investment behaviour and the life expenditure increased while investment decreased.

FINDINGS

The investment is a process of using present earning for the future. This paper had identified the role of Income tax regime 1 on tax payers to save and invest in certain investment options to save tax. The economics of this investment is that all these investment opportunities are government linked funds, Provident fund, national saving certificate or Life insurance corporation. It is a debt to the governments from the households that they bet two benefits, interest for the investment and tax exemptions.

In the Income tax regime, maximum tax exemptions permitted is Rs 1.5 L. In the first slab Rs 2.5 to Rs 5L and the tax benefit Rs 7500 while the same tax benefit was Rs 30000 in the tax slab for Rs 5-10L while the tax benefit was Rs 45000 for the more than Rs 10L. The average interest gained for the Rs 1.5L at 8% is Rs 12000. This shows that the investor was getting a return for the Rs 1.5 for the different tax slabs including the interest gained for the tax saving investments are , 13%. 28%, and 38%. This was a motivation for investment if the income come under the tax slab.

But the new regime is not compelling the investors to invest their saving to get the tax exemption for tax saving, but scaled the income into multiple slabs and the saving become option. Hence, the compulsion for a minimal investment is removed in the regime 2. Average tax commitment seemed to be reduced in the regime 2, but I reality, after considering the interest and tax exemption, the tax commitment is less in regime 1. It helps to gain a financial stability in future die to investment.

CONCLUSION

The results show that the olde regime withdrawal affected the saving and investment behaviour as there is no need to invest to get tax exemption. The returns of this investment are so good, It improves investment and the financial stability in the future.

This study has positive effect of the Income tax regime 1

in promoting saving investment culture among the tax payers. The real benefit

and tax commit has been discussed in detail that the first regime is a

motivation for financial budgeting, planning and investment. This shows that

the tax system has an influence on household investment.

ACKNOWLEDGMENTS

None.

REFERENCES

Abdeljawad, I., Alia, M. A., and Demaidi, M. (2023). Financing Constraints and Corporate Investment Decision: Evidence from an Emerging Economy. Competitiveness Review: An International Business Journal Incorporating Journal of Global Competitiveness, 34(1), 208–228. https://doi.org/10.1108/cr-02-2023-0033

Alfathya, N. A. F., Sumiati, N., and Indrawati, N. N. K. (2025). Understanding the Drivers of Investment Intention: A Systematic Literature Review. Asian Journal of Management Analytics, 4(3), 1151–1170. https://doi.org/10.55927/ajma.v4i3.14968

Child-Centred Investments to Achieve Targets of Vision 2025 by Department of Women Development and Child Welfare, Government of Telangana. (2020). [Report].

King, J., and Julian King & Associates Ltd. (2016). Value for Investment: A Practical Evaluation Theory [Book; PDF]. Julian King & Associates Ltd.

Mastufa Ahmed. (2024). 2025 Pay Raise and Salary Trends: A Comprehensive Guide. People Matters.

Peterson, Coulborn, Samuelson, Johnson, and Keynes. (2021). Inflation: Meaning and types.

Sahoo, T. (2020). Background for Section 80C of the Income Tax Act (India). Retrieved March 2, 2026.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© ShodhPrabandhan 2026. All Rights Reserved.